{kind=link}

In the complex landscape of financial planning, life insurance serves as a critical tool for ensuring the long-term financial security of beneficiaries. Among the myriad of options available, life insurance policies with long-term payouts have gained significant attention. These policies promise extended financial support, often touted as a superior choice for those seeking to provide a stable income stream for their loved ones over an extended period. However, the question remains: are these long-term payout policies inherently better than their counterparts with shorter payout durations? This article aims to dissect the various facets of life insurance policies with long-term payouts, weighing their advantages against potential drawbacks, and offering a balanced perspective to help individuals make informed decisions tailored to their unique financial goals and circumstances. Through an analytical lens, we will explore the intricacies of these policies, examining factors such as financial stability, inflation, and individual needs, to determine whether long-term payouts truly offer the most beneficial path forward in life insurance planning.

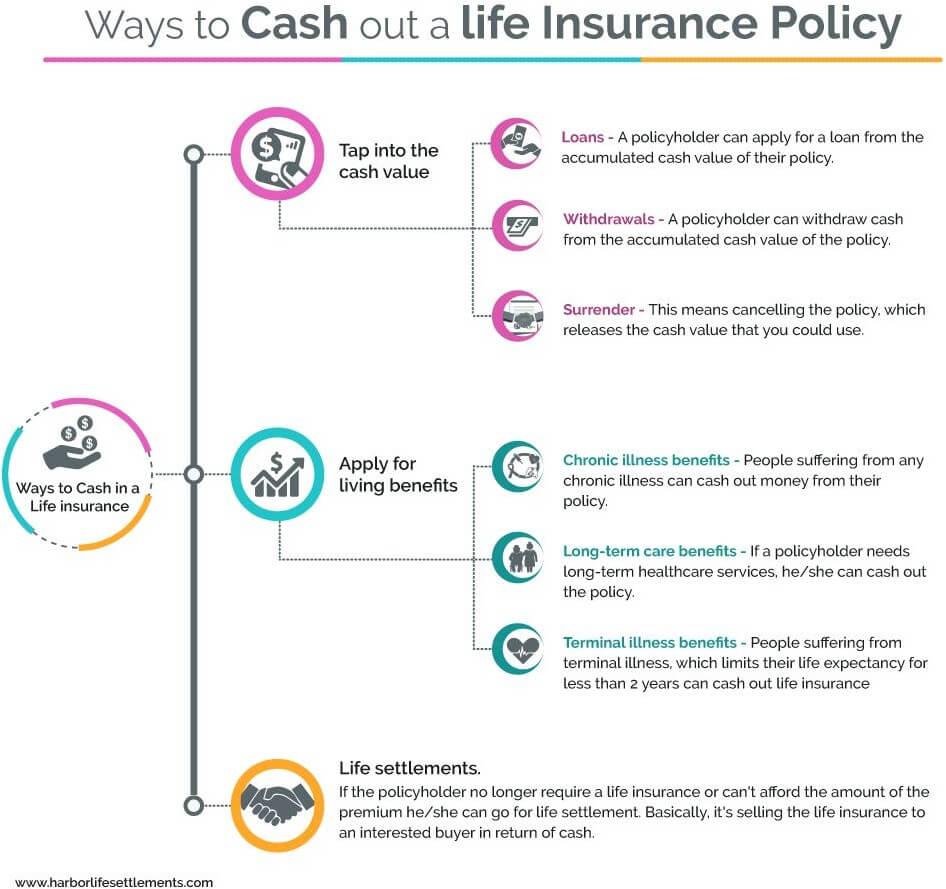

Evaluating the Benefits and Drawbacks of Long Term Payouts in Life Insurance

When considering life insurance policies with extended payout durations, it’s essential to weigh both their advantages and potential limitations. Long-term payouts can offer beneficiaries a steady income stream over several years, which can be particularly beneficial for those who may not be adept at managing large sums of money all at once. This approach can help ensure financial stability and provide a reliable income to cover ongoing expenses such as education, mortgage payments, or healthcare costs.

However, there are also drawbacks to consider. Long-term payout structures might limit the immediate access to funds that could be crucial in addressing urgent financial needs, such as settling debts or covering unexpected expenses. Additionally, the total payout over time might be less than a lump sum due to inflation and other economic factors. Furthermore, beneficiaries might find the administrative process more cumbersome, as they would need to manage the ongoing payouts and possibly deal with additional paperwork or legal considerations.

- Benefits: Financial stability, structured income, long-term planning

- Drawbacks: Limited immediate access, potential reduced value over time, administrative complexities

Understanding the Financial Implications of Extended Payout Structures

When evaluating life insurance policies, it’s crucial to consider the financial implications of extended payout structures. These plans, which disperse benefits over a prolonged period rather than a lump sum, can offer several advantages but also come with potential downsides. Extended payouts can provide beneficiaries with a steady income stream, helping them manage finances better over the long term and potentially reducing the temptation of spending the entire benefit at once. Additionally, these payouts can be structured to adjust for inflation, maintaining the purchasing power of the funds over time.

However, it’s important to weigh these benefits against certain challenges. Potential drawbacks of extended payout structures include:

- Interest Accumulation: The insurance company may hold onto a portion of the funds, earning interest, which could have otherwise benefited the beneficiaries.

- Loss of Flexibility: Beneficiaries might need access to larger sums of money for emergencies or significant expenses, which a fixed payout structure might not accommodate.

- Market Fluctuations: Depending on how the policy is structured, extended payouts might be subject to market risks, potentially impacting the total amount received.

Thus, while extended payout structures can be beneficial, they are not universally superior. It’s essential for policyholders to assess their unique financial situations and the needs of their beneficiaries when deciding on the appropriate payout structure.

Assessing the Suitability of Long Term Payouts for Different Financial Goals

When considering life insurance policies with long-term payouts, it’s crucial to evaluate their alignment with your specific financial objectives. Long-term payouts can offer a steady stream of income, which might be particularly beneficial for certain goals. However, not every financial plan will benefit equally from such arrangements. Here are some scenarios where long-term payouts might be advantageous:

- Retirement Planning: A consistent payout can supplement retirement income, providing a reliable cash flow to cover living expenses without the need to liquidate other assets.

- Education Funding: For families planning for their children’s education, long-term payouts can ensure funds are available when needed, potentially avoiding the need for student loans.

- Estate Planning: A structured payout can help in managing estate taxes and providing for beneficiaries over an extended period, aligning with long-term wealth transfer strategies.

Conversely, some goals may require a different approach. For instance, if your primary aim is to quickly eliminate debt or invest in high-return opportunities, a lump sum might be more appropriate. Flexibility is key; evaluating how long-term payouts fit within the broader context of your financial landscape is essential. Balancing immediate needs with future security often determines the best course of action.

Recommendations for Choosing the Right Life Insurance Payout Option

When navigating the myriad of life insurance payout options, it’s crucial to assess the unique needs and circumstances of your beneficiaries. Lump-sum payouts can offer immediate financial relief, helping cover expenses like funeral costs, outstanding debts, or mortgage payments. However, they require prudent financial management to ensure long-term security. On the other hand, installment or annuity payouts provide a steady income stream, which can be beneficial for beneficiaries who may not have experience managing large sums of money. This option can help ensure that funds are not depleted quickly, providing a safety net over time.

Consider the financial acumen and spending habits of your beneficiaries. If you opt for a long-term payout, evaluate the following:

– Financial stability: Are your beneficiaries financially savvy or do they need help managing money?

– Income needs: Would a regular income stream better support their lifestyle or financial obligations?

– Inflation protection: Does the payout option offer adjustments for inflation to maintain purchasing power?

Ultimately, the right choice hinges on aligning the payout structure with the financial habits and needs of your beneficiaries, ensuring they receive maximum benefit from the policy.