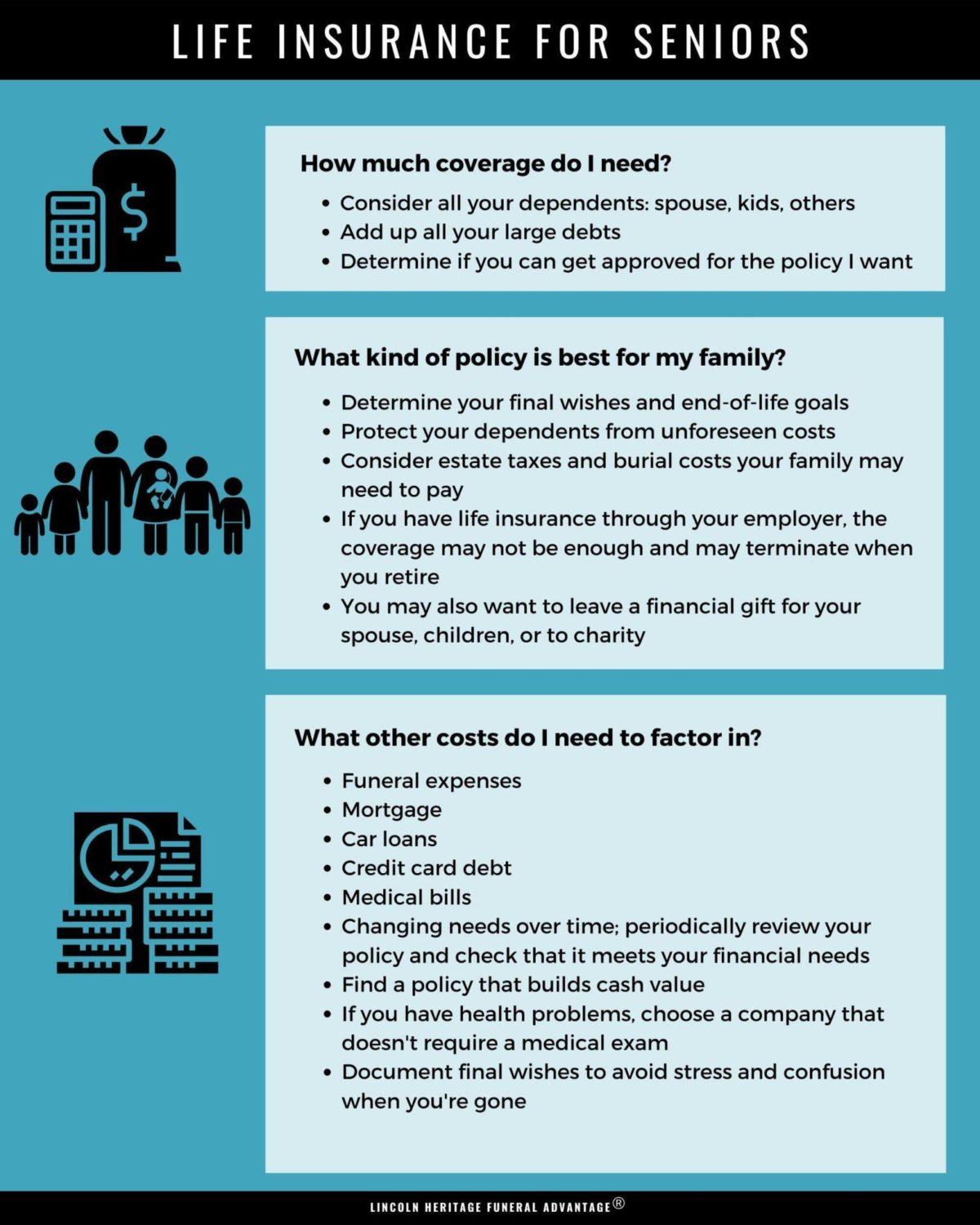

{kind=link}

Life insurance is often perceived as a financial safety net exclusively for breadwinners, designed to replace lost income and ensure the economic stability of dependents in the event of an untimely death. However, this narrow view overlooks the broader spectrum of individuals who contribute to a household’s well-being in non-monetary ways. In today’s evolving social and economic landscape, the importance of life insurance extends beyond the traditional wage earner. This article explores the multifaceted roles within a family unit that merit consideration for life insurance coverage, shedding light on how non-breadwinners—such as stay-at-home parents, caregivers, and even young adults—play pivotal roles that, if disrupted, could lead to significant financial and emotional strain. By examining the often overlooked value of these contributions, we aim to provide a comprehensive understanding of why life insurance should be an integral component of financial planning for every family member, regardless of their income-earning status.

Expanding the Scope of Life Insurance Coverage

Traditionally, life insurance has been associated primarily with the financial protection of families where one member is the main source of income. However, this conventional view is evolving. Today, life insurance is increasingly being recognized for its potential to safeguard the economic contributions of all family members, not just those who bring home a paycheck. Consider the invaluable yet often overlooked roles of stay-at-home parents and caregivers. Their daily efforts, from managing household responsibilities to providing childcare, represent significant economic value. In the event of their untimely absence, the costs to replace these services can be substantial. Life insurance for non-breadwinners ensures that these hidden contributions are acknowledged and covered, offering peace of mind to the entire family unit.

- Stay-at-home parents: Their role is crucial in maintaining the household and nurturing the family, often requiring substantial replacement costs for services such as childcare, cleaning, and meal preparation.

- Caregivers: Whether caring for aging parents or special needs family members, their support is irreplaceable, and life insurance can help cover potential expenses arising from their absence.

- Young adults and children: Though they may not yet contribute financially, insuring them can help cover future expenses and provide a financial cushion in the face of unexpected events.

By expanding life insurance coverage to include these essential yet frequently underestimated roles, families can better ensure comprehensive financial protection and stability.

Understanding the Financial Impact of Non-Breadwinners

While the primary focus often falls on the family’s main income earner, it’s crucial to recognize the financial contributions of those who aren’t traditional breadwinners. Their roles, whether as stay-at-home parents or part-time workers, have significant economic value that warrants protection. Consider the tasks they manage daily—childcare, household management, and transportation. These responsibilities, if outsourced, would incur substantial costs. By acknowledging this, families can better understand the potential financial strain in the absence of these contributions.

- Childcare costs can quickly escalate, impacting the family budget.

- Household duties, from cleaning to meal preparation, require time and resources.

- Managing schedules and transportation saves on logistical expenses.

Incorporating life insurance for non-breadwinners ensures that their indispensable roles are financially safeguarded. This strategy can provide a buffer for unforeseen expenses, allowing families to maintain their lifestyle and meet their obligations during challenging times.

Securing the Future: Life Insurance for Every Family Member

Life insurance is often associated with the family’s primary income earner, but its benefits extend far beyond this traditional role. In today’s dynamic world, every family member plays a vital part in the household’s financial ecosystem. Insuring all members, including non-working spouses, children, and even grandparents, can be a strategic move to secure the family’s financial future. While a non-working spouse might not bring in a paycheck, they contribute significantly through household management, childcare, and other essential tasks. If something unexpected were to happen, the cost of replacing these services could be substantial. Similarly, a policy for children can provide a financial cushion for unforeseen medical expenses or future educational needs.

- Non-working Spouses: Their contributions in managing the household are invaluable and often irreplaceable.

- Children: Coverage can assist with medical expenses or future educational investments.

- Grandparents: Their coverage can help with end-of-life expenses, easing the financial burden on the family.

By considering life insurance for each family member, you’re not just preparing for the unexpected; you’re investing in peace of mind. This approach ensures that all contributions, whether financial or otherwise, are recognized and protected. The goal is to build a robust safety net that supports the family through all of life’s uncertainties, creating a legacy of security and resilience for future generations.

Comprehensive Life Insurance Strategies for Modern Families

In today’s dynamic family structures, life insurance should be viewed as a versatile tool that extends beyond merely protecting the income of the primary earner. Modern families often consist of dual-income households, stay-at-home parents, and even extended family members living under one roof. In these scenarios, the absence of any family member can lead to financial strain, underscoring the importance of insuring all adults within the household. Life insurance can cover more than just the loss of income; it can also account for the value of unpaid work, such as childcare, household management, and elder care, which are critical to maintaining a family’s standard of living.

- Dual-income families: Protect both incomes to safeguard the family’s financial future.

- Stay-at-home parents: Insure to cover the cost of outsourced services they provide daily.

- Extended families: Consider policies for elderly members who may provide financial or caregiving support.

By adopting a holistic approach to life insurance, families can ensure that their financial plans are robust enough to withstand the unexpected loss of any member, thus preserving their lifestyle and future goals. Utilizing tailored strategies that reflect each family member’s unique contribution can transform life insurance from a mere safety net into a comprehensive financial strategy.