{kind=link}

When it comes to planning for the future, selecting the right life insurance policy is a crucial decision that can significantly impact both your financial security and peace of mind. With various options available, two of the most commonly considered types are term life insurance and whole life insurance. Each offers distinct features and benefits tailored to different needs and life stages. This article aims to demystify the complexities surrounding these two popular life insurance options, providing you with a clear understanding of their differences, advantages, and potential drawbacks. By examining the key factors involved, we will guide you in making an informed choice that aligns with your personal financial goals and family needs.

Understanding Term Life Insurance and Its Benefits

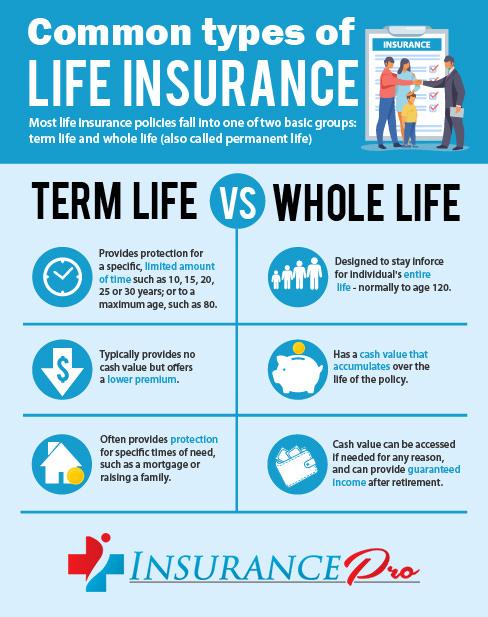

Term life insurance is a type of policy that provides coverage for a specific period, typically ranging from 10 to 30 years. It’s an attractive option for those seeking affordable protection, especially for individuals who want to secure their family’s financial future during critical life stages such as raising children or paying off a mortgage. One of the primary benefits of this insurance is its cost-effectiveness. Because it only offers a death benefit without any cash value accumulation, premiums are generally lower compared to whole life insurance. This makes it an ideal choice for budget-conscious individuals who need substantial coverage without the high costs.

Advantages of term life insurance include:

- Flexibility: Policies can be tailored to fit the length of time you expect to need coverage.

- Simplicity: It’s straightforward with no investment component, making it easy to understand.

- Convertibility: Many policies offer the option to convert to a permanent policy later on.

While term life insurance provides substantial benefits, it’s important to weigh these against your long-term financial goals and the need for potential cash value growth, which whole life insurance offers. Evaluating your personal circumstances and financial priorities will help you determine if term life insurance aligns with your needs.

Exploring Whole Life Insurance and Long-Term Advantages

Whole life insurance is a type of permanent insurance that provides coverage for the insured’s entire lifetime, as long as premiums are paid. Unlike term insurance, which only covers a specific period, whole life insurance comes with a cash value component that grows over time. This cash value is a significant feature, offering several long-term advantages:

- Guaranteed Death Benefit: The policy ensures a payout to beneficiaries upon the policyholder’s death, providing peace of mind and financial security.

- Cash Value Accumulation: Over time, the policy accumulates a cash value that can be borrowed against or withdrawn, offering a financial cushion for emergencies or opportunities.

- Stable Premiums: Whole life insurance premiums remain consistent throughout the policyholder’s life, making it easier to budget for long-term financial planning.

- Potential Dividends: Some whole life policies offer dividends, which can be used to reduce premiums, purchase additional coverage, or be taken as cash.

These features make whole life insurance an attractive option for individuals seeking lifelong coverage with the added benefit of a growing financial asset. However, it’s essential to weigh these advantages against personal financial goals and compare them with the benefits of term life insurance to determine the most suitable choice.

Comparing Costs and Flexibility of Term vs Whole Life Policies

When weighing the financial aspects of term and whole life insurance, it’s crucial to consider both the costs and flexibility each offers. Term life insurance is generally more affordable upfront, providing coverage for a specific period, typically ranging from 10 to 30 years. This makes it an appealing option for individuals seeking substantial coverage during crucial life stages such as raising children or paying off a mortgage. However, once the term expires, you may face higher premiums to renew or risk losing coverage altogether.

In contrast, whole life insurance comes with higher initial premiums but offers the advantage of lifelong coverage and a savings component known as cash value. This cash value grows over time and can be borrowed against, providing financial flexibility. Key considerations include:

- Term Life: Lower initial cost, fixed term, no cash value.

- Whole Life: Higher initial cost, lifelong coverage, cash value accumulation.

Guidelines for Making an Informed Decision on Life Insurance

When faced with the decision of selecting a life insurance policy, it’s essential to weigh your options carefully. Term life insurance is typically favored for its affordability and straightforward nature. It provides coverage for a specific period, usually ranging from 10 to 30 years, and is ideal for those seeking temporary protection. Key benefits include:

- Lower initial premiums compared to whole life insurance

- Simplicity in terms and conditions

- Flexibility to convert to a permanent policy if needed

On the other hand, whole life insurance offers lifelong coverage, often accompanied by a cash value component that grows over time. This option may suit those looking for long-term financial planning and stability. Consider the following advantages:

- Guaranteed death benefit and fixed premiums

- Potential for cash value accumulation

- Opportunity for policy loans against the cash value

Ultimately, the right choice hinges on your personal financial goals, family needs, and long-term planning strategy. Assess your situation carefully to make an informed decision.