{kind=link}

In today’s fast-paced world, young families are often caught in a whirlwind of responsibilities, from managing household expenses to planning for future milestones. Amidst these pressing concerns, life insurance frequently takes a backseat, perceived as a distant necessity for later years. However, prioritizing life insurance at an early stage can serve as a crucial foundation for financial stability and peace of mind. This article explores the reasons why life insurance should be a priority for young families, shedding light on its role in safeguarding loved ones, ensuring financial continuity, and providing a safety net against unforeseen events. By understanding the benefits and implications of life insurance, young families can make informed decisions that secure their future and protect their most valuable assets—their family members.

Understanding the Basics of Life Insurance for Young Families

For young families, navigating the world of life insurance can initially seem daunting. However, understanding its fundamentals is crucial for safeguarding your family’s financial future. Life insurance serves as a safety net, providing essential support to your loved ones in the event of unforeseen circumstances. Term life insurance and whole life insurance are the two primary types that families should consider. While term life insurance offers coverage for a specific period, whole life insurance provides lifelong protection and includes a savings component. Evaluating your family’s needs and financial goals will help determine which type aligns best with your circumstances.

- Term Life Insurance: Typically more affordable, with coverage for a set period.

- Whole Life Insurance: Offers lifetime coverage and a cash value component.

- Beneficiary Designation: Ensure your policy names the right beneficiaries to receive the benefits.

- Coverage Amount: Consider your family’s living expenses, debts, and future financial needs when choosing coverage.

The Financial Security Life Insurance Provides for Future Generations

In a world where uncertainties loom large, having a robust plan for the future becomes imperative, especially for young families. Life insurance stands as a cornerstone of financial stability, ensuring that the dreams and aspirations of future generations are not left to chance. By securing a policy early on, families can safeguard their financial well-being and provide a safety net that extends beyond their immediate needs.

Key benefits of life insurance for future generations include:

- Financial Protection: It offers a financial cushion, allowing families to maintain their standard of living even in the absence of a primary breadwinner.

- Educational Support: Ensures that children’s educational goals can be met, helping them pursue their dreams without financial hindrance.

- Inheritance Creation: Provides a means to leave a legacy, ensuring that wealth is passed down and can help future generations build a better life.

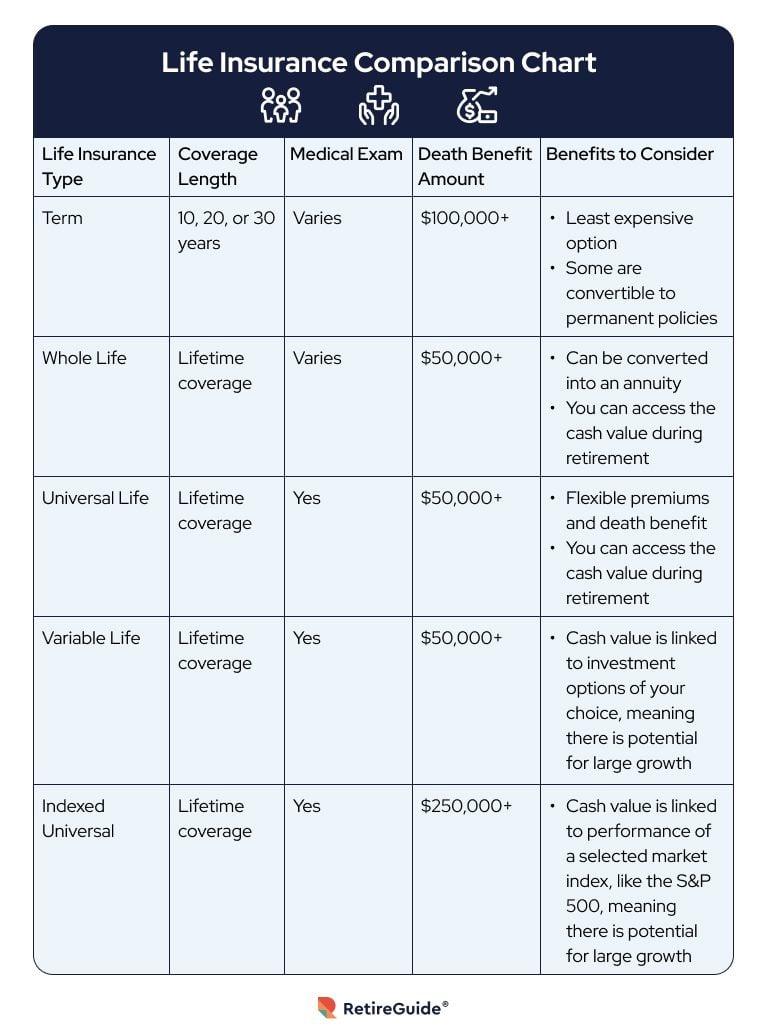

Evaluating Different Life Insurance Options to Suit Your Familys Needs

When considering life insurance, it’s essential to explore the diverse range of options available to find the best fit for your family’s unique circumstances. Each type of life insurance policy offers different benefits, and understanding these can help in making an informed decision. Here are some of the common life insurance options:

- Term Life Insurance: This is often the most straightforward and affordable option, providing coverage for a specified period. It’s ideal for young families seeking to cover significant expenses such as a mortgage or children’s education costs in the event of an untimely death.

- Whole Life Insurance: As a permanent policy, it not only offers lifelong coverage but also accumulates cash value over time. This can be a good choice if you’re looking for a policy that serves as both a protective measure and a financial investment.

- Universal Life Insurance: Offering flexible premiums and death benefits, this policy allows for adjustments as your financial situation changes. It’s beneficial for families who may need to modify their coverage as their life circumstances evolve.

- Variable Life Insurance: This policy combines life insurance with investment options, allowing the cash value to be invested in a variety of separate accounts. It’s suited for those comfortable with taking on more risk for potentially higher returns.

Each of these options carries its own set of advantages and considerations. Evaluating your family’s current and future needs, financial situation, and risk tolerance will guide you in selecting the most suitable life insurance policy. Consulting with a financial advisor can also provide clarity and direction, ensuring your family is adequately protected.

Steps to Integrate Life Insurance into Your Familys Financial Planning

Integrating life insurance into your family’s financial planning involves several strategic steps to ensure that your loved ones are financially secure. Begin by assessing your current financial situation, which includes reviewing income, debts, and ongoing expenses. Understanding these elements will help you determine the appropriate coverage amount needed. It’s essential to consider future financial goals, such as children’s education or mortgage payments, to tailor the policy effectively.

Next, explore different types of life insurance policies to find one that aligns with your family’s needs. Term life insurance is often favored by young families due to its affordability and simplicity, providing coverage for a specific period. Whole life insurance, on the other hand, offers lifelong protection and a cash value component. Consulting with a financial advisor can provide clarity on which policy best fits your family’s circumstances. Additionally, regularly reviewing and updating your policy ensures it continues to meet your evolving financial goals and family dynamics.